GB finished pig prices record marginal decline

By Felicity Rusk

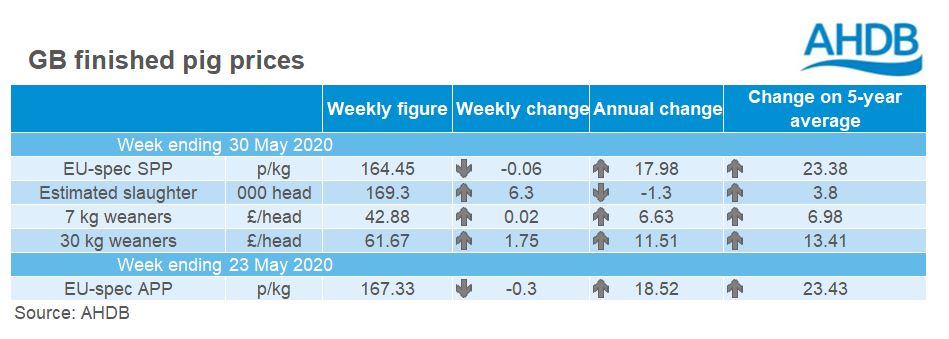

In the week ending 30 May, the EU-spec SPP paused its upward movement. Although the fall was relatively minor, at 0.06p, this is the first decline since early April. The price averaged 164.45p/kg, almost 18p above the same week last year. However, this time last year was when pig prices started to rise considerably, and so the year-on-year change has continued to erode.

Despite this week containing the Whitsun bank holiday, estimated slaughter continued to rise, totalling 169,300 head, 3.8% (6,300 head) more than in the previous week. This puts throughputs slightly below last year (-1,300 head). Reports continue to suggest that supplies are tight at present.

Demand was reported as good, likely supported by the dry weather encouraging BBQs. In the week ending 24 May, sales of primary pork, bacon and sausages continued to show strong growth.

Carcase weights were onaverage 210g lighter than in the previous week, at 84.80kg. Weights continue to track above last year, with carcases in the most recent week coming in 1.20kg heavier.

In the week ending 23 May, the EU-spec APP fell by 0.30p, to average 167.33p/kg. With the SPP moving in the opposite direction in the same week, the difference between the two narrowed to 2.82p.

Both 7kg weaner and 30kg store prices recorded an uplift in the week ending 30 May. Prices for 30kg weaners recorded an uplift of £1.75 to average £61.67/head. The 7kg price rise was considerably smaller at 2p on the week, to average £42.88/head. Reports suggest that supplies of both 30kg stores and 7kg weaners have been tight. Demand was reported as good, though there are growing concerns over the dry weather, which could lead to higher input costs.