AIMS Criticises FSA Chair’s Stance on Meat Inspection Charges

The Association of Independent Meat Suppliers (AIMS) has strongly opposed recent comments made by Professor Susan Jebb, Chair of the Food Standards Agency (FSA), regarding the UK’s meat inspection charging system.

AIMS argues that Professor Jebb’s characterisation of the existing discount system as a “subsidy” is both misleading and harmful to the UK meat industry.

During last week’s FSA Board meeting, Professor Jebb suggested that the discount system for meat inspection charges effectively subsidises the UK meat sector. However, Dr Jason Aldiss, Head of External Affairs at AIMS, dismissed this claim, stating: “It is our view that Professor Jebb’s portrayal of the discount system as a subsidy demonstrates a profound misunderstanding of the regulatory framework.”

Meat Industry Costs and Trade Barriers

Dr Aldiss explained that the current discounts are essential to offset what he described as “excessively bureaucratic and duplicative” charges that impose “exorbitant costs” on meat businesses. “The current FSA charges to the UK meat sector are among the highest in the world and, in effect, act as a state-sponsored trade barrier. This places domestic producers at a significant disadvantage in international markets,” he added.

AIMS is advocating for a switch to a headage-based charging system, which would align with global standards. Dr Aldiss believes this alternative would provide a fairer and more transparent way of calculating inspection costs, better reflecting the scale of operations and supporting competitiveness and sustainability within the UK meat industry.

Meat Inspections and Food Safety

Professor Jebb’s assertion that meat inspections are a “vital consumer protective function” has also been challenged. Dr Aldiss pointed to the European Food Safety Authority (EFSA), which has questioned the effectiveness of traditional meat inspection methods. According to EFSA, some current practices may fail to detect modern biological hazards and could even compromise food safety. “This raises critical questions about the allocation of resources and the necessity of current inspection protocols,” said Dr Aldiss.

Economic Impact on Small and Medium-Sized Enterprises

AIMS also rebuffed claims that meat inspection fees constitute only a minor cost to slaughterhouses. While these charges may seem small in relation to total turnover, Dr Aldiss emphasised their significant impact on net margins, particularly for small and medium-sized enterprises. “The financial burden of these fees threatens the viability of numerous businesses, undermining the broader agricultural economy,” he stated.

Call for Public Funding of Meat Inspections

AIMS further argued that if meat inspections are truly essential for public health, they should be publicly funded rather than financed through charges imposed on the industry. “If meat inspections are deemed a vital consumer protection measure — a position increasingly at odds with the evidence — it stands to reason that their funding should come from public taxation. This would ensure public health objectives are achieved without compromising the economic stability of the meat sector,” Dr Aldiss concluded.

The debate over meat inspection charges highlights ongoing tensions between regulatory authorities and industry stakeholders. AIMS is calling for urgent reforms to create a fairer, more sustainable system for UK meat producers, ensuring competitiveness in global markets while maintaining food safety standards.

Millers of Speyside Abattoir to Focus Solely on Beef Slaughtering Amid Rising Costs

The Millers of Speyside abattoir in Grantown will transition to solely a beef slaughtering facility starting next year. Managing director Sandy Milne cited labour shortages and rising operational costs as the primary reasons for this shift, making it necessary to streamline the business.

As part of this change, the abattoir will no longer offer private kill services for pork and lamb. However, arrangements have been made for pig private slaughter at Brechin abattoir when required. Milne explained that the business is outsourcing the supply of lamb and pork for their retail butchery customers and will focus exclusively on beef slaughtering from the start of the year.

Milne emphasized that the shortage of experienced labour and increasing running costs necessitated this decision. While private kill services for pork and lamb will be discontinued, the abattoir will continue to provide private kill facilities for cattle.

Deadweight pig prices in Ireland are on an upward trajectory in response to relatively tight supplies for slaughter. Prices have increased steadily week on week from a low of 190c/kg in mid February 2024. The average price paid for grade E pig prices in Ireland for the w/e 24th November was €2.03/kg excluding Vat. The current Irish price is 5c/kg lower than the corresponding week last year.

Throughput

While throughput has improved in the last quarter demand continues to run ahead of supplies. Total throughput YTD is 2,950,613 which is marginally behind the corresponding period in 2023.

The latest available data from the CSO shows that Irish exports of primary pigmeat products were valued at €243 million, 2% higher than the corresponding period in 2023.

A recovery in pig supplies for processing and a slight improvement in carcase weights have contributed to a similar 2% increase in export volumes during H1.

Within the H1 exports, there were notable increases in the value of trade to the UK (+16% to €71 million), and EU markets (+25% to €59 million). Meanwhile, there were declines in the value of Irish pigmeat exports to Asian markets (-15% to €77 million) and Oceania (-37% to €16 million.).

Base quotes from the major processors have improved slightly this week with €8.20/kg – €8.50/kg for well finished lambs (+QA bonus) on offer. With well fleshed lambs in demand, some major processors have also increased paid carcass weight limits, with all main plants paying for a 23-5kg carcass.

Relatively tight lamb supplies combined with some stability in demand from the domestic and export markets have contributed to this firming of the trade all year. Tighter lamb supplies are also a feature in other key lamb producing regions of Europe and the UK with the latest Eurostat figures indicating a contraction in breeding flock numbers in many regions.

The Irish ewe flock contracted by 3.7 per cent in the December 2023 census versus December 2022 levels. This decline in the ewe flock of 107,000 head is one factor contributing to the tightness in supplies currently.

Prices

Reported deadweight price for week ending the 8th of December increased by 26c/kg to €8.14/kg, reflective of the continuing improvement recorded in quoted prices from the major lamb processors. In the corresponding week in 2023 the reported deadweight price was €6.42/kg. The deadweight trade has also improved across the UK regions.

Reported spring lamb prices in mainland GB were the equivalent of €8.36/kg last week (+9c/kg) while in Northern Ireland there was a notable improvement in the trade to be €8.02/kg (+16c/kg).

Relatively tight supplies of lamb for slaughter in Northern Ireland combined with competition from the live export trade to both mainland GB and ROI contributed to this firming in the trade.

Southern Hemisphere prices remain well below European prices however they have improved significantly over the last few weeks, narrowing the price differential with the EU. With a lead time on product shipments this recent improvement in deadweight prices should impact their competitiveness on EU markets in the medium to longer term.

Prices this week took a jump and are at €5.52/kg and €4.47/kg for Australia and New Zealand , Australia’s price taking another jump by 17c/kg while New Zealand sees a slow down reducing of 5c/kg after a period of mostly week on week increases for the past 15 weeks.

Throughput

There was a decrease in the total sheep kill in DAFM approved plants last week to 41,265 head, compared to 59,714 the same week in 2023.

Tighter supplies has been a feature of the 2024 lamb season to date with a smaller lamb crop, a difficult lambing and changeable grass growing conditions all impacting lamb availability for processing. Total TYD slaughter is down 9% on 2023 to total 2,318,846 head.

There were 39,614 cattle processed in DAFM approved plants last week, a slight increase of 45head from the previous week.

Prime cattle throughput YTD is currently on par with the same period last year at 1,245,998 head although a notable tightening in prime cattle availability is expected as we move into the final quarter of the year. A contraction in cattle numbers on the ground and a lively export trade have contributed to this outlook with numbers expected to remain tight for much of 2025.

Average carcase weights also continue to trend below previous years with the combination of a challenging grass growing season and a growing dairy influence on the prime cattle kill playing a role in the decline. The downward trend in average carcase weights is expected to continue in the short to medium term with calf registrations to suckler cows continuing to decline, while the number of beef sired calves produced from the dairy herd continues to increase.

Prices

There was a lift in the steady base quotes at Irish meat plants this week in response to tighter supplies and an expected increase in retail and foodservice demand for the Christmas period. In general, producers were offered a base price of €5.45/kg for steers with reports of up to €5.50/kg available.

Starting quotes for heifers are in the region of €5.50/kg this week with similar room for negotiation being reported. The trade for young bulls was also described as steady, with prices of between €5.70/kg and €5.90/kg on-offer for R grading animals under 24 months of age.

The cow trade remains relatively steady, with well-fleshed O+ grading suckler cows being offered prices of €5.10-5.20/kg, while prices for O grading dairy cows generally range from €5.00-5.05/kg. A significant proportion of the cow kill have achieved a conformation score of P in recent months and the prices available for these animals vary significantly based on grade, weight and quality.

For the week ending 8th of December 2024, the average price paid by Irish beef processors for R3 increased slightly by 2c/kg to be at €5.47/kg. This remained 63c/kg ahead the corresponding week in 2023 when the R3 steer price was €4.83/kg. Note that reported prices exclude VAT but include all bonus payments such as in-spec bonus, breed-based producer groups etc.

EU and UK prices

Across the EU, the average reported price for R3 grading young bulls was €5.62/kg (excluding VAT) for the week ending 8th December, 2024. This is 67c higher than Week 49 of2023 whenprices averaged €4.95/kg for this category.

In the UK, tighter cattle supplies and firm demand have meant deadweight beef prices have continued to firm. This week the average UK R3 steer price increased by 3c/kg to €6.52/kg.

Stability has returned to the cattle market, reflecting the balancing act between supply and demand.

Market confidence has continued to trend upward despite the weather conditions in Victoria and SA.

Slaughter has been very consistent and remains the highlight of the year.

After a turbulent 2023, the cattle market got back on its feet during 2024. The beef herd has now reached maturity, leading to more beef in domestic and international markets. 2024 has been marked by three key themes:

Stability

Confidence

Stronger supply.

Stability

Without a doubt, the cattle market has stabilised – reflecting the balancing act between supply and demand which are influenced by weather, overall confidence and increased female slaughter, among many other factors.

Prices over the last 12 months have lifted by 20–39%, indicating the recovery of the market from the challenging conditions in 2023. The current prices are now tracking 1–20% below the 10-year average and reflect the substantial recovery the cattle market has shown over a short period of time.

Over the last year, Australia experienced two different seasonal conditions split across the south and the north. The seasonal conditions in pastoral regions in SA and western Victoria drove increased turn-off. As a result, NSW and Queensland producers benefited from this turn-off due to their favourable seasonal conditions.

Market confidence has certainly shifted from last year – many would say last year was the first time in a long time that producers made a decision based on a forecast rather than actual weather events. This confidence influenced buying behaviour; however, despite poor conditions in Victoria and SA, prices remained strong due to demand from NSW and Queensland producers.

All eyes have been on the global market, particularly the United States, which has recorded the lowest cattle herd in about 70 years. This has driven high cattle prices and thus increased the volume exported.

Stronger supply

Supply has remained steady over the past 12 months, with weekly slaughter capacity averaging 130,000 head a week according to the National Livestock Reporting Service (NLRS). The second half of the year averaged slightly higher at 140,000 head a week. Slaughter in 2024 is tracking just above the 10-year average and is around 16% above the 5-year average.

Processing capacity has increased by around 20% over the past four years, indicating the impact of the Pacific Australian Labour Mobility (PALM) scheme and other labour schemes which have significantly grown processing capacity.

Attribute to Emily Tan, MLA Market Information Analyst

Another Arrest in Food Crime Probe

NFCU officers, together with Dyfed-Powys Police, attended a farm in Wales on Wednesday 4 December 2024 and arrested one man.

“Officers from the National Food Crime Unit, working with Dyfed-Powys Police, arrested a 52 year old man from West Wales on suspicion of conspiracy to supply unfit meat, as part of an investigation into alleged illegal and unsafe meat.

Smokies are a food safety issue as they aren’t produced under hygienic conditions, and they are illegal because the meat still has its skin on and lacks traceability. We are advising people to steer clear of sheep meat produced in this way as it may be a health risk, and to contact their local Trading Standards or us if they suspect smokies are being produced or sold.

If we find any unsafe food on the market, we will take action to protect the public. If you suspect food crime, report it to Food Crime Confidential always available on food.gov.uk or by phoning 0800 028 1180.”

Neil Castle, Deputy Head of the FSA’s NFCU

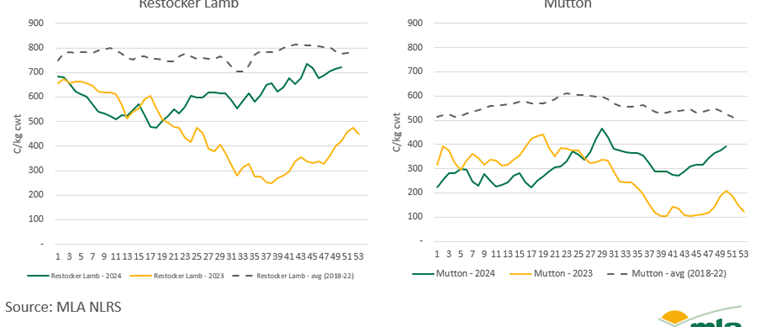

A year in review: the Australian sheep and lamb market

Key points:

Following the volatile market last year, producers acted cautiously in 2024.

Differing conditions across the country promoted trade and competition.

Record production was driven by strong export demand.

2024 has been a year of recovery, nervousness and record production. Compared to the previous 12 months, the sheep and lamb market has shown strength and stability. However, when we look further back, unpredictability and volatility have continued to impact producers across the country.

Cautiousness

Coming out of an extremely volatile market, the sheep and lamb sector entered the new year in seeming recovery. Driven by a positive summer across much of the east coast, markets reflected a move beyond the confidence and climate-impacted 2023. The market, however, did not remain in recovery, and instead fell more dramatically than the previous year. Producer sentiment in May reached +4, remaining 22 points below the previous year. This initial volatility impacted producer confidence in the market as well as trading decisions. Cautiousness remained through the year as prices lifted in the autumn market and continued as prices surpassed the 2023 market.

As the year continued, quality had the largest impact on price. This reflects a market before recent history, where liquidation and rebuild have driven supply and demand influences. The Australian flock was sitting at its largest in over a decade. Strong supply, partnered with solid international and domestic demand, led to record export volumes. Growth in both established and emerging markets shows that as the top exporter of sheepmeat, Australia has been able to keep up with our improving production.

Strong export demand has maintained competition in the domestic livestock market. This demand has caused market protection across the country as conditions have varied dramatically.

Regions across SA, Victoria, and NSW have experienced extremely tough conditions. Faced with a positive summer season, many producers started the year well. However, conditions dried up fast and hard, placing producers in a position of possibly being overstocked and relying on feed. Alternately, central and northern NSW and sheep pastoral zones generally experienced positive conditions, creating an environment that supported quality and promoted trading. This has led to a very strong year-end as finished lamb prices have remained firm much later than the seasonal norm.

WA continued to operate differently from eastern states without the support of close markets. The state began the year on a low base as dry conditions impacted joining and selling decisions. Turn-off and individual destocking led to a surplus of stock.

There were two main outcomes:

Prices did not see the same recovery as the eastern market.

For a period, more animals were turned off than could be absorbed by domestic processors.

This price and stock availability caused a significant movement of stock out of the state, with commentary noting WA animals were travelling even beyond neighbouring SA.

Production

Production of lamb and mutton has skyrocketed thanks to supply and a growth in processor capacity. Looking into weekly slaughter, initially, 2024 followed regular seasonal trends; however, focusing on the tail end of this year, there has been a clear new focus for processors.

Mutton volumes have lifted dramatically across the country, indicating strength in our export market demand but also an indication of producer decision making. Across WA, the proportion of mutton over lamb is relatively high, showing that producers may be eating into their breeding flock. On the east coast, all states have lifted their production mutton, especially NSW, which just last week processed more than 50% of mutton on lamb, which hasn’t been done since 2007.

Producers are becoming more efficient in production and are able to produce more lambs from less due to genetic, fertility and breed investments. With the reduction of wool production, dry conditions, a large ewe flock, and generally firm mutton prices, decisions have been made around the retention of older stock.

The processing sector’s ability to keep up with the sheep supply is growing. Finishing off with some numbers, based on the year-to-date National Livestock Reporting Service (NLRS) slaughter volumes, combined sheep and lamb slaughter – adjusted up to account for an approximate 20% coverage gap of the NLRS – we have processed more than 37 million sheep and lambs in 2024, with three weeks to go. Australia has not surpassed 35 million in a total calendar year before, enforcing how capable the sector is to absorb a new normal of production.

Looking ahead to 2025

The past 12 months have demonstrated the ability of the sheep sector to recover. An elevated flock, strong supply of stock, and even stronger supplies of sheepmeat, have been absorbed into the domestic and international production systems. Australia is operating in an elevated state which is likely to remain into 2025. Without predicting any extreme climatic conditions (wet or dry), we are likely to continue to produce elevated levels of sheep and lamb.

Three things to keep an eye on into 2025:

growing international markets, including the emerging UK and India FTA opportunities

the United States protein situation, which will impact more than just cattle and beef

breed dynamics – the growth of shedding sheep and the move away from Merinos and wool – how will this impact sheepmeat production moving forward?

Attribute to: Erin Lukey, MLA Senior Market Information Analyst

Tired of Turkey? Try These Alternative Christmas Meats

The Best Alternative Christmas Meats to Buy if You Don’t Want Turkey

For many, turkey has become synonymous with Christmas, but it’s not everyone’s cup of tea. Whether you’re looking to switch things up or cater to a family that isn’t fond of turkey, the good news is that there are plenty of fantastic alternatives that can add flavour and flair to your festive table.

Here are some of the best alternative meats to consider for Christmas this year:

1. Goose

Goose is a classic Christmas meat, particularly in the UK before turkey took the spotlight. It’s a richer, fattier bird that offers a succulent, deep flavour. The bonus of choosing goose is the generous amount of fat it renders, perfect for crispy roast potatoes. The meat has a lovely, gamey taste that pairs well with traditional Christmas trimmings like red cabbage, apples, and even chestnuts.

2. Duck

Duck is another bird that works well for Christmas. It has a distinctive flavour that’s more intense than turkey but not as rich as goose. The juicy meat and crispy skin make it a hit at festive dinners. Serve it roasted with seasonal vegetables and a fruity sauce, like plum or orange, to bring out the best of its flavour.

3. Beef

Roast Beef

Roast beef is an excellent alternative for those who prefer red meat. A prime rib or a beef tenderloin can make for a spectacular centrepiece, offering a hearty, robust flavour that pairs beautifully with Yorkshire puddings and all the Christmas trimmings. The beauty of beef is its versatility – whether you like it rare or well-done, it can easily be tailored to your taste.

4. Lamb

Lamb offers a tender, flavourful option that can bring a Mediterranean twist to your Christmas feast. A leg of lamb, roasted with garlic, rosemary, and thyme, makes for a succulent and aromatic meal. Its rich flavour complements sides like roasted root vegetables, mint sauce, and even a dash of pomegranate for a festive touch.

Roast Lamb

5. Pork

A roast pork joint, especially one with crackling, is a show-stopper at Christmas. It’s an indulgent, juicy choice that pairs well with apple sauce and roasted veggies. Consider a glazed ham for a more traditional touch – honey, mustard, and cloves work perfectly to give your pork a festive sweetness that everyone will enjoy.

6. Venison

For something a little more adventurous, venison is a superb choice. Its gamey flavour, lean texture, and seasonal appeal make it an excellent alternative to turkey. Roast venison, cooked with juniper berries or red wine, can make a truly elegant Christmas meal. Serve with roasted vegetables and a rich sauce to enhance the flavour.

7. Chicken

If you’re after something simple and familiar, a free-range roast chicken can be a great alternative to turkey. It’s versatile, widely available, and easier to manage in smaller households. Plus, chicken can be jazzed up with festive stuffing, crispy skin, and all the usual trimmings for a Christmas meal that’s both traditional and delicious.

8. Gammon

A glazed gammon joint is a favourite for many during the festive season. Slow-cooked and then roasted with a sweet glaze, such as honey or marmalade, gammon offers a rich and satisfying flavour. It can be served hot as the main event or cold alongside other meats for a Christmas Day buffet. The salty-sweet taste of gammon pairs perfectly with mustard, pickles, and roasted potatoes.

9. Pheasant

For a touch of something unique, pheasant is a traditional British game bird that’s lighter than duck or goose but still full of flavour. It’s ideal if you want to offer your guests something a little different. Serve it roasted with seasonal fruits like pears or cranberries to highlight its delicate, gamey taste.

Tips for Choosing Your Alternative Meat

Consider the size of your gathering: Some meats, like goose or beef, are better suited for larger crowds, while chicken or pheasant work well for smaller parties.

Think about flavour: If you want something richer and more indulgent, meats like duck, lamb, or venison are ideal. For something more subtle, consider chicken or gammon.

Don’t forget the sides: Whatever meat you choose, remember that festive side dishes – from crispy roast potatoes to rich gravies – can elevate your meal to the next level.

Christmas is the perfect time to experiment with different meats and create new traditions around the table. Whether you go for the gamey richness of venison, the tenderness of roast beef, or the classic appeal of a glazed ham, there’s no reason to feel tied to turkey.

Whichever meat you choose, the festive spirit and a beautifully set table are what truly make Christmas dinner special.